Interchange + Vs. Flat Rate Pricing Structures in Payment Processing

Understand the different pricing models in the merchant services industry and see how your business can save on transaction fees by choosing the right pricing model.

Greg Turner | Merchant Services & POS Solutions Expert

8/15/20243 min read

Understanding Interchange Plus vs. Flat Rate Pricing Models in Merchant Services

In the merchant services industry, business owners have several pricing models to choose from when processing credit card transactions. Among these, the two most common are the interchange plus pricing model and the flat rate pricing model. Each has its pros and cons, and understanding the differences between them can significantly impact a business's bottom line.

What is Interchange Plus?

Interchange plus pricing is a transparent pricing model where the business pays the interchange fee set by the card networks (Visa, MasterCard, etc.) plus a fixed markup. The interchange fee is a non-negotiable cost set by the card networks and varies based on factors such as the type of card used (e.g., rewards cards typically have higher fees) and whether the transaction is card-present or card-not-present.

For example, a merchant might pay an interchange fee of 1.8% + $0.10 per transaction and a markup of 0.2% + $0.05 per transaction. In this case, the total fee for a $100 transaction would be:

Interchange Fee: 1.8% of $100 = $1.80 + $0.10 = $1.90

Markup: 0.2% of $100 = $0.20 + $0.05 = $0.25

Total Fee: $1.90 + $0.25 = $2.15 (or 2.15%)

The key advantage of interchange plus pricing is its transparency. Businesses know exactly what they're paying in interchange fees and the processor’s markup, making it easier to understand and optimize costs.

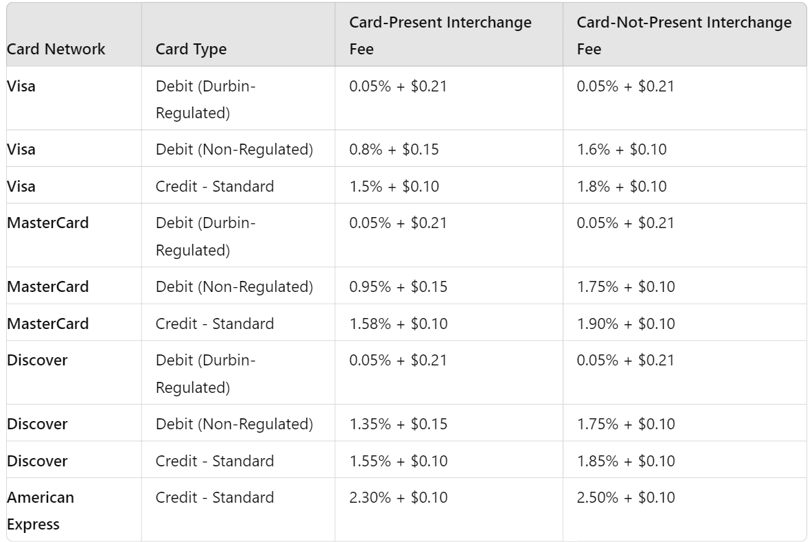

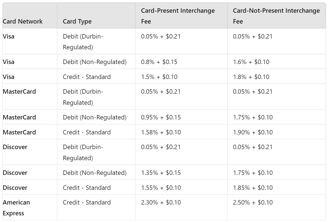

Here's an updated 2024 table that reflects the impact of the Durbin Amendment on debit card transaction fees for financial institutions with $10 billion or more in assets:

Notes on Durbin-amendment:

Durbin-Regulated Debit: Applies to financial institutions with $10 billion or more in assets. The interchange fee is capped at 0.05% of the transaction value plus a fixed fee of $0.21 per transaction.

Non-Regulated Debit: Applies to smaller financial institutions with less than $10 billion in assets, where standard interchange fees still apply.

What is Flat Rate Pricing?

Flat rate pricing, on the other hand, offers simplicity by charging a single, consistent fee for all transactions, regardless of the card type or the transaction method. This fee is typically a percentage of the transaction amount, sometimes with an additional fixed fee.

For example, a payment processor might charge a flat rate of 2.9% + $0.30 per transaction. For the same $100 transaction, the fee would be:

Total Fee: 2.9% of $100 = $2.90 + $0.30 = $3.20 (or 3.2%)

Flat rate pricing is popular for its simplicity. Businesses can predict their costs more easily since they pay the same fee for every transaction. This model is often favored by small businesses and those who prefer a straightforward billing structure.

Comparing and Contrasting Interchange Plus and Flat Rate Pricing

Cost Structure:

Interchange Plus: Costs vary depending on the card type and transaction method. While the interchange fee can fluctuate, the markup remains constant. This can lead to savings, especially if a business processes a lot of debit or card-present transactions with lower interchange rates.

Flat Rate: The cost is consistent, making it predictable but often higher, especially for businesses with a mix of low-cost transactions. The flat rate generally covers the worst-case scenario, leading to higher average costs for the merchant.

Transparency:

Interchange Plus: Highly transparent. Merchants can see the exact interchange fees and processor markups, making it easier to identify cost-saving opportunities.

Flat Rate: Less transparent. The simplicity comes at the cost of visibility into what portion of the fee goes to interchange and what goes to the processor.

Suitability for Different Businesses:

Interchange Plus: Ideal for businesses with a high volume of card-present transactions, where the interchange fee is generally lower. It benefits businesses that want to optimize costs and are comfortable with a variable fee structure.

Flat Rate: Best for businesses that prefer simplicity and predictability in their pricing, or those with low transaction volumes where the ease of understanding fees outweighs potential savings.

Why Interchange Plus Can Be More Cost-Effective

Square, Stripe, and Other Flat Rate Processors: Companies like Square and Stripe have popularized the flat rate model, typically charging around 2.9% + $0.30 per transaction. This rate is convenient but tends to be higher than what many businesses could achieve with interchange plus pricing, particularly those that process a high volume of card-present transactions.

Potential Savings with Interchange Plus: By opting for an interchange plus model with a modest markup, businesses can often pay closer to 2% in transaction fees. This is especially true for businesses where most transactions are card-present, as these transactions generally have lower interchange rates. Over time, the savings from lower transaction fees can add up, making interchange plus an attractive option for cost-conscious businesses.

Conclusion

Both interchange plus and flat rate pricing models have their place in the merchant services industry. The choice between them should be guided by the specific needs and transaction profiles of the business. While flat rate pricing offers simplicity and predictability, interchange plus can provide significant cost savings for businesses willing to navigate a more variable fee structure. Understanding these differences can help business owners make informed decisions and optimize their payment processing costs.

Need help picking what's right for you? Get help from one of our experts by getting in touch below.

Get in touch

Contact us:

248-930-8096

info@prosperitypayments.co

M-F-9-5

© 2002. All rights reserved.